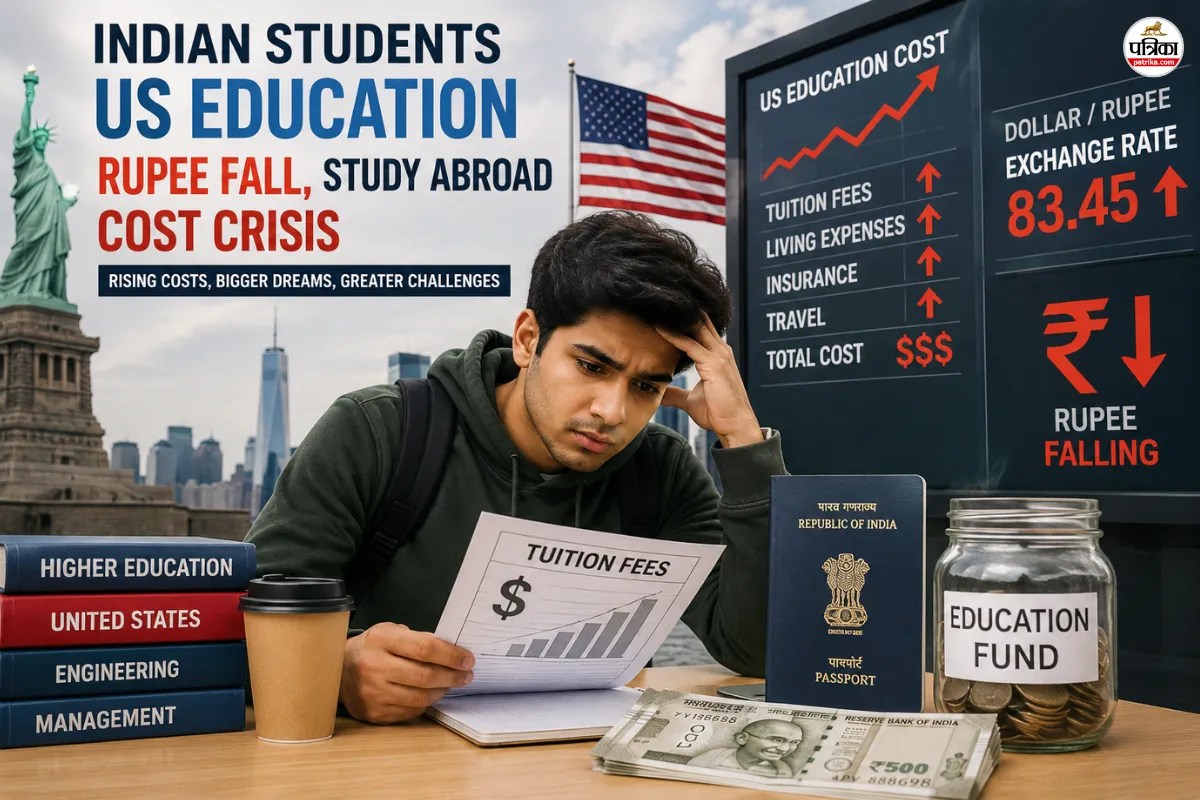

The headlines are bleeding. Every major news outlet is currently running the same tired narrative: "Rupee hits record low," followed by a sob story about an Indian student in Chicago who now has to trade their weekend Starbucks for instant noodles. They want you to believe that a 3% or 4% currency fluctuation is a structural disaster for your education.

They are wrong. In fact, they are looking at the wrong side of the ledger.

If you are treating your US education as a "cost" to be managed in INR, you’ve already lost the game. A fluctuating exchange rate isn’t a crisis; it’s a filter. It separates the students who are "spending" from the professionals who are "investing." If a ₹3 shift against the Dollar breaks your financial back, the problem isn’t the Reserve Bank of India. The problem is your ROI calculation.

The Tuition Trap and the Myth of the Fixed Cost

The standard argument suggests that as the Rupee weakens, the "burden" on Indian families increases. This assumes that the money used to pay for a degree is a sunk cost that never returns.

Let’s look at the math. The average starting salary for a STEM graduate in the US ranges from $75,000 to $105,000. When the Rupee weakens, yes, your immediate tuition payment in Mumbai terms goes up. But so does the value of every single Dollar you will earn during your OPT (Optional Practical Training) and beyond.

If you pay your fees while $1 equals ₹83, but you start earning and sending money back when $1 equals ₹88, you are effectively shorting the Rupee and winning. You are paying in "cheaper" present-day Rupees and reaping rewards in "stronger" future Dollars. Over a three-year H-1B stint, that currency delta doesn’t just cover the extra tuition cost; it wipes it out entirely.

Stop looking at the check you’re writing today. Start looking at the remittance you’re sending tomorrow.

Arbitrage is the Only Real Subject You Need to Learn

The most successful Indian students I’ve mentored over the last decade don’t complain about exchange rates. They exploit them.

The "lazy consensus" says you should wait for the Rupee to "stabilize" before transferring funds. This is a gambler’s fallacy. Currency markets are a random walk in the short term. Trying to time the USD-INR pair to save 50 paise on a $20,000 transfer is a waste of intellectual capital.

Instead of obsessing over the rate, obsess over the Arbitrage of Skill.

The real "economic burden" isn't the exchange rate; it's the opportunity cost of staying in a market where the wage ceiling is significantly lower. A software engineer in Bengaluru might earn ₹25 Lakhs. That same engineer in Austin earns $120,000. Even with a "weak" Rupee, the purchasing power parity and the ability to service debt are vastly superior in the US.

Why a Weak Rupee is Your Competitive Advantage

Think about the psychology of the market. When the Rupee dips, the "tourist students"—those going for the "experience" or the "brand name" without a clear path to employment—start to panic. They withdraw applications. They settle for local universities.

This is your opening.

- Reduced Competition: As the price of entry rises, the pool of applicants thins out.

- Focus: Financial pressure forces you to prioritize high-ROI majors over "fluff" electives.

- Aggressive Networking: When you know each credit hour costs more, you don’t skip class, and you don’t skip career fairs.

The Debt Delusion

"But the loans! The interest is killing us!"

I’ve seen families liquidate gold and ancestral land because they fear a 10% dip in the Rupee. This is emotional, not financial, decision-making.

If you have a loan in INR, a weakening Rupee is technically a challenge for repayment if you return to India immediately. But if you are staying in the US to work, you are earning in the very currency that is "crushing" you. Your debt becomes easier to service because you are paying back an INR-denominated loan with high-value Dollars.

Let’s run a thought experiment.

Imagine you take a ₹50 Lakh loan. At the start, that’s roughly $60,000.

Two years later, the Rupee crashes. Now, $60,000 is worth ₹55 Lakhs.

If you are working in the US, you only need to send back a fraction of your $9,000 monthly paycheck to cover the EMI. The "weak" Rupee actually makes your Indian debt shrink in real Dollar terms.

The media calls this a "burden." I call it a "devaluation of your liabilities."

The "Middle-Class Crisis" is a Planning Failure

The articles you read are designed to trigger anxiety in middle-class parents. They paint a picture of a student stranded in New York because the exchange rate moved 2%.

If a 2% move strands you, your buffer was non-existent. Professional-grade financial planning for US education requires a 15% currency volatility buffer. If you didn't build that in, you weren't "hit by the Rupee"; you were hit by your own lack of a margin of safety.

Stop blaming the macroeconomics for micro-level failures.

Stop Asking These Questions:

- "When will the Rupee get stronger?" (It won't. The long-term trend of emerging market currencies against the USD is a downward slope. Accept it.)

- "Should I wait a semester?" (No. Time in the market beats timing the currency.)

Start Asking These:

- "Does my chosen university have a high placement rate for H-1B sponsors?"

- "Can I offset the currency dip by working as a Teaching Assistant (TA) or Research Assistant (RA)?" (These roles often pay in USD and waive tuition—the ultimate hedge.)

The Brutal Truth About "Economic Burden"

The real economic burden isn't the cost of the Dollar. It’s the cost of mediocrity.

If you go to a third-tier US university, get a degree in a saturated field, and fail to land a high-paying job, the exchange rate will indeed ruin you. But it would have ruined you at ₹70 to the Dollar just as easily as at ₹85. The currency is just the scapegoat for a bad investment.

The US is the most expensive playground in the world. It is also the highest-paying. If you are worried about the "price of the ticket," you aren't ready for the "stakes of the game."

The Rupee "falling" is merely the market's way of asking: How badly do you want to be here?

If your answer is "I'm worried about the price of my latte," then stay home. The Indian economy is growing, and there are plenty of opportunities in Mumbai or Delhi. But if you want the global stage, stop whining about the exchange rate. It is a rounding error in the career of a high-performer.

The Dollar isn't getting more expensive. Your ambition is just getting its first real stress test.

Pass it or pack up. There is no middle ground.